Definition and Purpose

Escrow is commonly associated with real estate transactions, but it can be used in any scenario where funds are transferred from one party to another. With real estate, escrow can be used when purchasing a home or for the life of a mortgage. The use of escrow has been on the rise as a way to offer secure transactions for high-ticket items, such as stocks, art, jewellery, antiques or intellectual property like software source code.

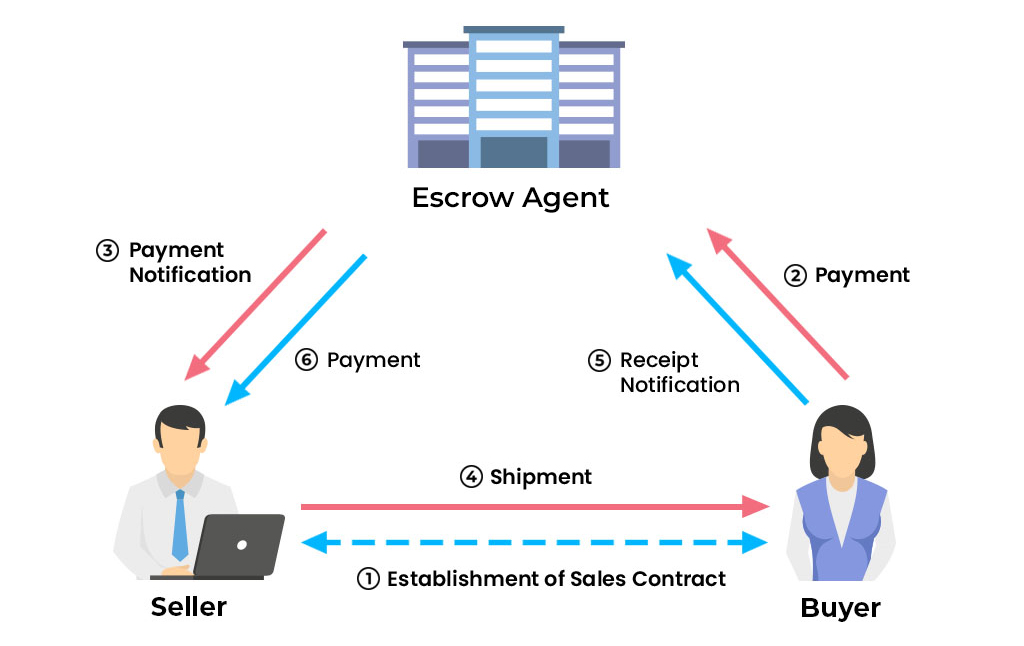

Escrow Transaction Flow

Escrow Transaction Flow Diagram

Step-by-Step Process

Step 1: Agreement

Buyer and Seller agree to the terms and conditions of the transaction.

Step 2: Fund Deposit

The Buyer deposits funds into the escrow account.

Step 3: Notification

The escrow agent informs the Seller that money has been deposited into the Escrow account.

Step 4: Delivery/Service

Seller ships the product to the Buyer or performs the requested service.

Step 5: Receipt Confirmation

The Buyer receives the product or service and confirms satisfaction.

Step 6: Fund Release

The escrow agent releases funds to the Seller from the escrow account.

Types of Escrow Accounts in Indian Banking

1. Real Estate Escrow

Used in property transactions to hold earnest money, down payments, and closing costs until all conditions are met.

Example: A buyer deposits ₹10 lakh in escrow while purchasing a property. The money is released to the seller only after title verification and completion of all legal formalities.

2. Mortgage Escrow

Banks collect additional monthly payments for property taxes and insurance, holding them in escrow until these bills are due.

Example: A home loan borrower pays an extra ₹5,000 monthly into escrow for property tax and insurance premiums.

3. Business Transaction Escrow

Used in mergers, acquisitions, and large business deals to ensure compliance with terms before fund transfer.

4. Online Transaction Escrow

Digital platforms use escrow services for high-value online purchases to protect both buyers and sellers.

Regulatory Framework in India

Reserve Bank of India (RBI) Guidelines

RBI regulates escrow accounts under the Banking Regulation Act, 1949. Banks must maintain proper documentation and comply with KYC norms for escrow account holders.

SEBI Regulations

For securities transactions, SEBI (Securities and Exchange Board of India) has specific guidelines for escrow accounts used in IPOs and other capital market transactions.

Real Estate (Regulation and Development) Act, 2016 (RERA)

RERA mandates developers to deposit 70% of funds received from buyers in a separate escrow account to be used only for construction of that particular project.

Benefits of Escrow Accounts

For Buyers

- Security: Funds are protected until goods/services are delivered as agreed

- Dispute Resolution: Neutral third party can mediate in case of conflicts

- Quality Assurance: Payment is released only after satisfaction

- Legal Protection: Formal documentation protects legal interests

For Sellers

- Payment Guarantee: Assurance that buyer has funds available

- Reduced Risk: Protection against payment defaults

- Professional Handling: Third-party management reduces administrative burden

- Trust Building: Increases buyer confidence in transactions

Escrow Account Features

Key Characteristics

- Neutral Third Party: Escrow agent must be independent of both parties

- Conditional Release: Funds released only upon meeting predetermined conditions

- Documentation: All terms and conditions must be clearly documented

- Time-bound: Usually has specific timelines for completion

- Interest Bearing: May earn interest depending on account type and duration

Common Applications in Indian Context

1. Infrastructure Projects

Government contracts often use escrow accounts to ensure proper fund utilization and project completion.

2. Import-Export Transactions

International trade transactions use escrow to mitigate risks associated with cross-border payments.

3. IPO and Capital Market

Companies going public deposit IPO proceeds in escrow accounts until listing requirements are met.

4. Insurance Claims

Large insurance settlements may be held in escrow pending final documentation and approvals.

Challenges and Limitations

Cost Factor

Escrow services involve fees that may range from 0.5% to 2% of the transaction value, making them expensive for small transactions.

Time Delays

The verification and approval process can delay transactions, especially in time-sensitive deals.

Limited Availability

Not all banks offer comprehensive escrow services, particularly for specialized transactions.

Digital Transformation

Fintech Integration

Modern escrow services are increasingly digitized with features like:

- Online account opening and management

- Real-time transaction tracking

- Automated condition verification

- Digital documentation and signatures

- Integration with payment gateways